|

|

CENTERS FOR MEDICARE &

MEDICAID SERVICES Medicare &You

2007 This is the official government handbook with important information about what’s new. what’s covered. health plans. prescription drug plans. your rights.

Welcome to Medicare & You 2007 Medicare is helping you stay healthy and active. The program offers you more than ever. More of you are taking advantage of the many preventive services that Medicare covers, and an unprecedented number of you have a prescription drug plan. Medicare is committed to providing information and tools to help you make the best health decisions for your individual needs. www.MyMedicare.gov is an exciting new service on the web. With this tool, you can see your health care claims, track which preventive services you need, and get the most up-to-date details about how to get the most out of your Medicare benefits. If you don’t have access to the web, the same information is available by calling 1-800-MEDICARE and through Medicare’s many partners in the community. That’s just the start. Medicare is working harder than ever to improve the information you can get. Better information means you can compare and choose better care for better prices. It means helping you access new treatments and innovative practices. As always, help is available anytime, day or night. You can visit www.medicare.gov or call 1-800-MEDICARE (1-800-633-4227). Medicare is also present in your local communities to get you the answers you need. Thank you for taking time to look at this Medicare handbook.

Michael O. Leavitt Leslie V. Norwalk, Esq. Secretary Acting Administrator Department of Health and Centers for Medicare & Human Services Medicaid Services

Medicare Basics

+

Part D You can choose this coverage. Private companies approved by Medicare run these plans. Plans cover different drugs. Medically necessary drugs must be covered.

+ Medigap (Medicare Supplement Insurance) Policy You can choose to buy this private coverage (or an employer/union may offer similar coverage) to fill in gaps in Part A and Part B coverage. Costs vary by policy and company. A Brief Look at Medicare Medicare is health insurance for people age 65 or older, under age 65 with certain disabilities, and any age with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a kidney transplant). Most people get their Medicare health care coverage in one of two ways. Your costs vary depending on your plan, coverage, and the services you use. OR

Part D Most Part C plans cover prescription drugs. If they don’t, you may be able to choose this coverage. Plans cover different drugs. Medically necessary drugs must be covered. For information about The Original Medicare Plan, see pages 25–32. Medicare Advantage Plans, see pages 33–42. Medicare prescription drug coverage, see pages 43–56. Other Medicare plans, see pages 58–59.

Medicare Basics What’s new or important in Medicare for 2007? What You Pay for Medicare—See the 2007 amounts on pages 101–104. Part B Premium—If you file an individual tax return and your yearly income is above $80,000 (or $160,000 for a married couple filing a joint tax return), your monthly Part B premium will be higher than the standard premium amount. For more information, see page 11. Medicare Advantage Plans (Part C) (like HMOs and PPOs)—

Information on these plans starts on page 33. Medicare Prescription Drug Plans (Part D)—Information on these plans starts on page 43. Outpatient physical and occupational therapy, and speech-language pathology—There may be limits in 2007, see page 103. Medicare Medical Savings Account (MSA) Plans—MSAs are a new way to get your Medicare health care, see page 39.

“Medicare & You 2007” explains the Medicare Program. It isn’t a legal document. The official Medicare Program provisions are contained in the relevant laws, regulations, and rulings.

Medicare Basics Where can I get help or more information? Visit www.medicare.gov on the web. Call 1-800-MEDICARE (1-800-633-4227) to get help in English, Spanish, and other languages. TTY users should call 1-877-486-2048. Register for MyMedicare.gov on the web. You can access the Medicare information you need on the web at any time. View claims, order forms and publications, and more (see page 89). If you don’t have a computer, Medicare’s partners can help you access this tool. Call your State Health Insurance Assistance Program for free counseling about choosing plans, buying a Medigap policy, and your Medicare rights, including appeals (see pages 92–95 for their telephone number). Medicare works with many organizations around the country and in your local community. For a more detailed list of telephone numbers and places to get personalized help, see pages 89–95.

How do I find information I need in this handbook? 1 Look at the “Table of Contents,” or 2 Look at the “List of Topics (Index)” that starts on page 1. This alphabetical list of specific topics is the easiest way to find information.

Blue words in the text are defined on pages 97–100.

Medicare Basics

If You’re New to Medicare...

“To Do” List

�

Decide how you want to get Medicare coverage, see pages 23–24.

�

Check pages 63–70 to see about help paying health care costs.

�

Check if current insurance works with Medicare, see pages 60–61.

�

Schedule a “Welcome to Medicare” physical exam, see page 17. � Ask your doctor what preventive services you should get, see page 12. � Consider Medicare prescription drug coverage, see pages 43–56. If you have employer or union coverage, see page 50. � Write important telephone numbers on the inside back cover. � Register at www.MyMedicare.gov to access personalized information, see page 89.

Table of Contents

Section 1

Section 3

Section 5 Pages

List of Topics (Index)............................................................1–6 What’s Covered What Is Medicare Part A? ......................................................................7–8 Medicare Part A-Covered Services and Items ..........................................9 What Is Medicare Part B? ..................................................................10–11 Medicare Part B-Covered Services and Items ..................................12–20 What Isn’t Covered....................................................................................21 Deciding How to Get Your Medicare Benefits ....23–24 Original Medicare Plan What it Is and How it Works ..............................................................25–26 Your Costs in the Original Medicare Plan ..............................................26 What Is “Assignment” and Why Is it Important? ..................................27 Adding Prescription Drug Coverage to the Original Medicare Plan ....28 Buying a Medigap (Medicare Supplement Insurance) Policy ........29–31 How Your Bills Get Paid If You Have Other Health Insurance......31–32 Other Options to Consider..............................................................32 Medicare Advantage Plans (Part C)

What Are Medicare Advantage Plans (like HMOs and PPOs)? ............33

(Continued)

Table of Contents

Section 6

Section 8

Section 9

Section 12

Pages

Medicare Prescription Drug Coverage (Part D)........43–56 Other Medicare Plans, Government, and Private Insurance ..............................................................57–62 Help for People with Limited Income and Resources ..............................................................................63–70 How to Join and Switch Plans ....................................71–78 Your Medicare Rights ......................................................79–88 For More Information

Get Personalized Medicare Information Anytime

..............................89 A more detailed listing of topics in this handbook starts on the next page. The information in this handbook was correct when it was printed. Changes may occur after printing. Visit www.medicare.gov on the web or call 1-800-MEDICARE (1-800-633-4227) to get the most current information. TTY users should call 1-877-486-2048. List of Topics (Index)

A

Acupuncture ..........................................21 B

Balance Exam ......................................16

Benefit Period ..........................97, 9, 102 Benzodiazepines....................................53 Bills (Claims)

Part A ..........26–27, 31–32, 80, 87, 89

Part C ..........................................41–42 C Cancer Drugs ........................................18 Cardiovascular Screenings....................13 Catastrophic Coverage..........................45 Check-up (see Physical Exam)..17, 15, 21 Chiropractic Services ....................13, 21 Cholesterol Screening ..........................13 Claims (see Bills) ........26–27, 31–32, 89 Clinical Breast Exam (see Pap Test)....17

Section 1: List of Topics (Index)

C (continued) Clinical Laboratory Services....13, 21, 103 Clinical Trials ........................................13 COBRA ..........................................61, 11 Coinsurance..........97, 25, 35, 44, 102–103 Colonoscopy..........................................14 Colorectal Cancer Screenings ..............14 Complaints (Appeals)..........8, 79–85, 12 Comprehensive Outpatient Rehabilitation Facility ........................81 Conditional Payment ............................31 Consolidated Omnibus Budget Reconciliation Act (COBRA) ........61, 11 Coordination of Benefits Contractor................................32, 42, 91 Copayment ..97, 25, 33, 35, 44, 102–103 Cosmetic Surgery..................................21 Costs 2007 ........................................101–104 Assignment ................................27, 26 Coinsurance ..97, 25, 35, 44, 102–103 Copayment ....97, 25, 33, 35, 102–103 Deductible......97, 10, 21, 25, 40, 44, 103 Help with Costs..........................63–70 Coverage (see Covered Services) ..9, 12–20 Coverage Determination (Part D)......93, 81 Coverage Gap ................................45, 44, 53 Covered Services (Part A & B) ................................9, 12–20 Creditable Prescription Drug Coverage..97, 47, 49, 50, 61, 72–73, 100 C (continued) Critical Access Hospitals..............97, 7, 9 CT Scans ..............................................19 Custodial Care....................7, 21, 98, 100 D Deductible ........97, 10, 25, 40, 44, 64, 103 Definitions ....................................97–100 Demonstrations/Pilot Programs ....59, 86 Dental Care ....................................21, 35 Dentures ................................................21 Department of Defense ........................91 Department of Health and Human Services (Office of the Inspector General) ..................................86–87, 91 Department of Veterans Affairs......................................24, 60, 91 Dialysis (Kidney Dialysis)..16, 34, 71, 74 Diabetes........................14–15, 17, 21, 38 Disabled..........................8, 38, 47, 68, 72 Discrimination ......................................88 Dispute (see Complaints) ....8, 79–85, 12 Doctor/Physician Services..................................10, 15, 103 Donut Hole (see Coverage Gap)..........45, 44, 53, 55 Drug Plan (see Medicare Prescription Drug Plan) ..................99, 28, 43–56, 23 Drugs (prescription)..........18, 21, 28, 36, 43–56 Durable Medical Equipment (like wheelchairs) ....9, 15, 16, 102–103

Section 1: List of Topics (Index)

E EKGs ....................................................19 Emergency Room Services......15, 33, 78 Employer/Union Drug Coverage..61, 50, 19, 31, 41, 43, 47, 97 Employer/Union Health Coverage................61, 11, 31, 41, 50, 72, 97 End-Stage Renal Disease (ESRD) ............................16, 34, 71, 74 Erectile Dysfunction Drugs ......................53 Exception ................................98, 53–54, 82 Extra Help Paying

Medicare Drug Costs ................64–65, 49

Medical Costs....................................66–67 F Fecal Occult Blood Test........................14 Federal Employee Health

Benefits Program (FEHBP) ........59, 51 G Generic Drugs ................................53–55 Glaucoma Testing..................................15 Grief Counseling ....................................9 Group Health Plan ......61, 11, 19, 31, 41 H Health Maintenance Organization (HMO) ..98, 33–34, 37, 71–78, 80, 100 Hearing Aids ............................16, 21, 23 Hearing Exams ........................16, 21, 35 Help..................................63–70, 81, 89–95 Hepatitis B Shot ....................................16 HMO........98, 33–34, 37, 71–78, 80, 100 Home Health Care ....9, 16, 81, 102–103 Hospice Care ............................9, 81, 102 Hospital Bed ..............................9, 15, 16 Hospital (care, inpatient

coverage)..................7, 9, 81, 97–98, 101 I Identity Theft ........................................86 ID Theft Hotline....................................86 Immunosuppressive Drug Therapy......19 Income-based (Part B) Premium ........11 Inspector General’s Hotline............86–87 Institution......................98, 38, 49, 54, 72 Internet ..................................................89 J Joining/Switching Plans ......71–78, 34, 51 K Kidney Dialysis..................16, 34, 71, 74 Kidney Transplant..19, 16–17, 34, 71, 74 L Lab Services (see Clinical Laboratory Services)................................13, 21, 103 Late Enrollment Penalty (see Part B, Part C, or Part D Penalty)

Section 1: List of Topics (Index)

L (continued) M Mammogram ..................................16, 37 Medicaid ............98, 66, 49, 64, 69, 71–72 Medical Equipment ......9, 15–16, 102–103 Medically Necessary..98, 9–10, 12–19, 54 Medical Nutrition Therapy ..................17 Medicare Advantage

Plans ....................98, 23, 33–42, 71–78 Prescription Coverage..35–38, 40–41, 99 Medicare-Approved Amount ........................98, 27, 102–104 Medicare Beneficiary Ombudsman ....85 Medicare Card......................7, 25, 89–91 Medicare Cost Plan ....................99, 58, 43 Medicare Helpline ................................90 Medicare Medical Savings Account (MSA) Plans ....................99, 39, 35, 43 Medicare Part A ......7–9, 21, 25, 101–102 Medicare Part B ......10–21, 25, 101, 103 Medicare Part C ................33–42, 94, 104 Medicare Part D..................43–56, 28, 104 Medicare Prescription Drug Coverage ..................43–56, 35, 40, 104 Medicare Prescription Drug

Plans ..................99, 28, 43–56, 23, 104 M (continued) Medicare Savings Programs ....67, 49, 64 Medicare SELECT ..........................75 Medicare Summary Notice ..................26, 79–80, 83, 87, 89 Medigap (Medicare Supplement

Insurance) Policies ....99, 11, 29–31, 74 N National Average Benchmark

Premium (Part D) ......................48, 104 O Occupational Therapy ........103, 9, 16–17 Office for Civil Rights ..................88, 91 Office of Personnel Management ........59 Office of the Inspector General..86–88, 91 Original Medicare

Plan ..................................99, 23–32, 77

Costs ............................26–27, 101–103

Section 1: List of Topics (Index)

P PACE (Programs of All-inclusive Care for the Elderly) ....................69, 59 Pap Test............................................17, 37 Part A (Hospital Insurance) ..7–9, 21, 25, 33–35, 40, 102 Premium........................................8, 101 Part B (Medical Insurance) ..........10–21, 33–35, 25, 103 Penalty ..................................10, 99, 101 Premium ..8, 10, 11, 35, 41, 44, 99, 101

Part C................................98, 33–41, 104 Part D ..........................35, 23, 28, 43–56 Penalty ......47–48, 30, 50–51, 73, 95, 104 Premium ..47, 36, 43, 56, 101–104, 104 Pelvic Exam ....................................17, 37 Penalty ......99, 10, 30, 43, 47–51, 61, 73 Phone Numbers ..90–95, inside back cover Physical Exams ........................15, 17, 21 Physical Therapy ................9, 16, 18, 102 Pilot Programs ................................59, 86 Pneumococcal Shot ..............................18 Point-of-Service Option ................99, 37 PPO ........................99, 36, 33–34, 23, 43 Practitioner Services ............................18 Preferred Provider Organization (PPO) Plan ....99, 36, 33–34, 43, 71–78 Premium ..........99, 101, 11, 35–37, 43, 56 P (continued) Prescription Drugs....................18, 21, 28, 36, 43–56 Preventive Services....99, 10–18, 89, 103 Primary Care Doctor........99, 36–37, 100 Prior Authorization ........................54, 97 Privacy Practices ............................83–84 Private Fee-for-Service (PFFS) Plans................................100, 35, 37, 43 Private Insurance ............................61–62 Programs of All-inclusive Care

for the Elderly (PACE) ................69, 59 Q Quality ................................8, 12, 23, 89 Quality Improvement

Organization ..............................8, 12, 90 R Railroad Retirement Board (RRB)......................7, 10, 90–91 Referral ............................100, 23, 36–37 Regional Preferred Provider

Organization..................................36, 78

Section 1: List of Topics (Index)

S

Second Surgical Opinions ....................18 (SNF) Care ..............100, 9, 81, 97, 102 Smoking Cessation ..............................18 Social Security ......7–8, 10–11, 65, 68, 91 Special Enrollment Period ..100, 10, 61, 73 Special Needs Plan ................100, 38, 74 Specialist ........................................36–37 Speech Language Pathology Services ............................9, 16, 19, 103 State Children’s Health Insurance Program..............................63 State Health Insurance Assistance Program ................................92–95, 100 State Insurance Department ................90 State Medical Assistance(Medicaid) Office......................................65–70, 90 Step Therapy..........................................54 Subluxation............................................13 Supplement Policy (see Medigap Policies)................99, 11, 29–31, 35, 74 Supplemental Security

Income (SSI) ..........................68, 64, 49

Diabetic ..................................15, 21, 27 T Telemedicine ................................100, 19 Telephone

Numbers ........90–95, inside back cover U Union Coverage..61, 11, 19, 31, 41, 43, 50, 75 Urgently Needed Care..............19, 33, 82 V Vaccinations (shots) ..........15, 16, 18, 21 Veterans’ Benefits (VA) ....60, 24, 51, 91 W Walker ..................................9, 15, 16, 90 Web ........................................................89 “Welcome to Medicare”

Physical Examination ........................17 X

X-ray ......................................................19

Medicare covers certain medical services and items in hospitals and other settings. Some are covered under Medicare Part A, and some are covered under Medicare Part B. As long as you have both Part A and Part B, these services and items are covered whether you have the Original Medicare Plan, or you belong to a Medicare Advantage Plan (like an HMO or PPO). What Is Medicare Part A? Part A helps cover your inpatient care in hospitals. This includes critical access hospitals and skilled nursing facilities (not custodial or long-term care). It also helps cover hospice care and home health care. You must meet certain conditions to get these benefits. If you aren’t sure if you have Part A, look on your red, white, and blue Medicare card (see sample card below). If you have Part A, “HOSPITAL (PART A)” is printed on your card. Note: Your card may be slightly different. It’s still valid.

Blue words in the text are defined on pages 97–100. Do you need to replace your Medicare card? If your Medicare card is lost or damaged, you can order a new card at www.socialsecurity.gov on the web. Or, call Social Security at 1-800-772-1213. TTY users should call 1-800-325-0778. If you get benefits from the Railroad Retirement Board (RRB), call your local RRB office or 1-800-808-0772, or visit www.rrb.gov on the web and select “Benefit Online Services.”

Section 2: What’s Covered What Is Medicare Part A? (continued) Cost: Most people automatically get Part A coverage without having to pay a monthly payment, called a premium. This is because they or a spouse paid Medicare taxes while working. If you don’t automatically get premium-free Part A, you may be able to buy it if

For most people, if you buy Part A coverage, you must also enroll in Part B and pay the Part B premium. If you have limited income and resources, your state may help you pay for Part A and/or Part B (see page 67). For more information, visit www.socialsecurity.gov on the web or call Social Security at 1-800-772-1213. TTY users should call 1-800-325-0778.

Section 2: What’s Covered Medicare Part A Helps Cover Your Medically-Necessary...

For specific costs and other information about these services, see pages

101–104.

Section 2: What’s Covered What is Medicare Part B? Part B helps cover medical services like doctors’ services, outpatient care, and other medical services that Part A doesn’t cover. Part B is optional. Part B helps pay for covered medical services and items when they are medically necessary (see pages 12–19). Part B also covers some preventive services. Cost: You pay the Part B premium each month (see page 101 for the 2007 amount). In some cases, this amount may be higher if you didn’t sign up for Part B when you first became eligible. You also pay a Part B deductible each year before Medicare starts to pay its share. See page 103 for the 2007 amount. You may be able to get help from your state to pay this premium and deductible (see page 67).

If you don’t take Part B when you are first eligible, the cost of Part B will go up 10% for each full 12-month period that you could have had Part B but didn’t sign up for it, except in special cases (see Special Enrollment Period on page 100). You may have to pay this penalty as long as you have Part B. If you didn’t sign up for Part B when you first became eligible, call Social Security at 1-800-772-1213 to see when you can apply. TTY users should call 1-800-325-0778. If you get benefits from the Railroad Retirement Board (RRB), call your local RRB office or 1-800-808-0772. Medicare Part B and TRICARE Coverage If you have TRICARE, you must have Medicare Part B to keep this coverage. However, if you are an active duty service member, or the spouse or dependent child of an active duty service member, you may not have to get Medicare Part B right away. You can get Part B during a Special Enrollment Period, and in most cases you won’t have to pay a late enrollment penalty.

Section 2: What’s Covered Medicare Part B and Group Health Plan Coverage from an Employer or Union Your Part B enrollment rights can be affected if you have coverage through an employer or union, and you or your spouse are still working, or if you have COBRA coverage (see page 61). Your decision about when to sign up for Part B can also affect your rights to buy a Medigap (Medicare Supplement Insurance) policy. For more information about enrolling in Part B, call Social Security (see previous page). You may also visit www.medicare.gov on the web and view the booklet “Enrolling in Medicare” or call 1-800-MEDICARE (1-800-633-4227) to ask questions. TTY users should call 1-877-486-2048. NEW As of January 1, 2007, Your Part B Premium is Based on Your Income Most people will pay the standard monthly Part B premium. However, some people will pay a higher premium based on their modified adjusted gross income. Your monthly premium will be higher if you file an individual tax return and your annual income is more than $80,000, or if you are married (file a joint tax return) and your annual income is more than $160,000. These amounts change each year. For the 2007 premium amount in your income range, see page 101. If you file an individual tax return and your income is above $80,000, or if you are married and file a joint tax return and your income is above $160,000, Social Security will use the income reported two years ago on your IRS income tax return to determine your premium (if unavailable, SSA will use income from three years ago). For example, the income reported on your 2005 tax return will be used to determine your monthly Part B premium in 2007. If your income has decreased since 2005, you can ask that the income from a more recent tax year be used to determine your premium, but you must meet certain criteria. At the end of each year, Social Security will send you a letter if your Part B premium will increase based on the level of your income and to tell you what you can do if you disagree. For more information about Part B premiums based on income, call Social Security at 1-800-772-1213. TTY users should call 1-800-325-0778.

Section 2: What’s Covered Part B Helps Cover These Items and Services Part B covers certain medical items and services no matter how you get your Medicare health care. Costs for these services vary depending on the plan you choose. More specific costs and other information about these services are on page 103. For most of these items and services, you must pay a copayment or coinsurance, and a deductible may apply. On pages 13–19 is an alphabetical list of common items and services Medicare covers if they are either: Medically necessary—This means the item or service is needed for the diagnosis or treatment of your medical condition, or Medicare-covered preventive services—like exams, lab tests, and screening shots to help prevent, find, or manage a medical problem. Preventive services may find health problems early when treatment works best. Talk to your doctor about which preventive services you need and if you meet the criteria for coverage.

You can live a healthy lifestyle by exercising, eating well, keeping a healthy weight, not smoking, and using preventive services. For a list of what isn’t covered, see page 21.

If you have a question or complaint about the quality of a Medicare-covered service, call your local Quality Improvement Organization. Visit www.medicare.gov, or call 1-800-MEDICARE (1-800-633-4227) to get their telephone number. TTY users should call 1-877-486-2048.

This symbol identifies the preventive services in the Part B coverage charts on pages 13–19. Section 2: What’s Covered Medicare Part B Helps Cover...

Note: Coinsurance and/or deductibles may apply. Preventive Service

Medicare Part B Helps Cover...

Colorectal To help find precancerous growths, and help prevent or find cancer Cancer early, when treatment is most effective. One or more of the following Screenings tests may be covered. Talk to your doctor. 1 Fecal Occult Blood Test—Once every 12 months if age 50 or older. You pay nothing for the test, but usually have to pay for the doctor visit. 2 Flexible Sigmoidoscopy—Generally, once every 48 months if age 50 or older, or every 120 months when used instead of a colonoscopy for those not at high risk. 3 Screening Colonoscopy—Once every 120 months (high risk every 24 months). No minimum age. 4 Barium Enema—Once every 48 months if age 50 or older (high risk every 24 months) when used instead of sigmoidoscopy or colonoscopy.

Your risk for colorectal cancer increases if you or a close relative have had colorectal polyps or cancer, or if you have inflammatory bowel disease (like Crohn’s disease). In 2007, Medicare covers its share of these costs even if you haven’t met the yearly Part B deductible. Diabetes To check for diabetes. These screenings are covered if you have any of Screenings the following risk factors: high blood pressure (hypertension), dyslipidemia (history of abnormal cholesterol and triglyceride levels), obesity, or a history of high blood sugar. Tests are covered if you answer yes to two or more of the following questions. Are you age 65 or older? Are you overweight? Do you have a family history of diabetes (parents, brothers, sisters)? Do you have a history of gestational diabetes (diabetes during

pregnancy), or did you deliver a baby weighing more than 9 pounds? Based on the results of these tests, you may be eligible for up to two diabetes screenings every year. Note: Coinsurance and/or deductibles may apply. Preventive Service

Section 2: What’s Covered Medicare Part B Helps Cover...

Note:

Medicare Part B Helps Cover...

Note: Coinsurance and/or deductibles may apply. Preventive Service

Section 2: What’s Covered Medicare Part B Helps Cover...

Note: Coinsurance and/or deductibles may apply. Preventive Service

Medicare Part B Helps Cover...

Note: Coinsurance and/or deductibles may apply. Preventive Service

Section 2: What’s Covered Medicare Part B Helps Cover...

Note:

Coinsurance

and/or

deductibles

may

apply.

Section 2: What’s Covered For More Information About Medicare Part B Covered Items and Services If you have the Original Medicare Plan and need more information about any of the listed items or services, any items or services you need that aren’t listed, or information about your share of the costs, visit www.medicare.gov on the web and select “Search Tools” at the top of the page. Then select “Find Out What Medicare Covers.” Or call

1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048. For more information about coverage in Medicare Advantage Plans (like HMOs or PPOs) under Part C, see pages 33–42. For information about Medicare prescription drug coverage (Part D), see pages 43–56.

You may have the right to appeal decisions about health care payment or services. See Section 10 for more information about your appeal rights. Section 2: What’s Covered

What isn’t covered by Medicare Part A and Part B? Medicare doesn’t cover everything. Items and services that aren’t covered include, but aren’t limited to the following: Acupuncture Chiropractic services (except as listed on page 13) Cosmetic surgery Custodial care (help with bathing, dressing, using the bathroom, and eating) at home or in a nursing home Deductibles, coinsurance, or copayments when you get certain health care services (see pages 101–104) (People with limited income or resources may get help paying these costs, see pages 63–70.) Dental care and dentures (with only a few exceptions) Diabetic supplies (some, like syringes or insulin, unless the insulin is used with an insulin pump or unless you get Medicare coverage for prescription drugs [Part D]) Eye care (routine exam), eye refractions and most eyeglasses (see page 15) Foot care (routine) such as cutting of corns or calluses (with only a few exceptions) Hearing aids and hearing exams for the purpose of fitting a hearing aid Hearing tests that haven’t been ordered by your doctor Laboratory tests (screening) except those listed on pages 13–19 Long-term care, such as custodial care in a nursing home Orthopedic shoes (with only a few exceptions) Physical exams (routine or yearly) (Medicare will cover a one-time physical exam within the first six months you have Part B, see page 17.) Prescription drugs—most prescription drugs aren’t covered by Medicare Part A or Part B. See Section 6 for information about adding Medicare coverage for prescription drugs (Part D). Shots (preventive vaccinations) except those listed on pages 13–19 Tests (screening) except as listed on pages 13–19 Travel (Health care you get while traveling outside of the United States, except as listed on page 19.)

Section 2: What’s Covered Notes

Deciding How to Get

You can choose different ways to get the services covered by Medicare. Depending on where you live, you may have different choices. In most cases, when you first get Medicare, you are in the Original Medicare Plan. You may want to consider a Medicare Prescription Drug Plan to add drug coverage. Or, you may want to consider a Medicare Advantage Plan (like an HMO or PPO) that provides all your Part A, Part B, and often Part D coverage. You make a choice when you are first eligible for Medicare. Each year you can review your health and prescription needs and switch to a different plan in the fall. There are things you should consider to help you meet your needs.

Things to Consider for Each Option Cost—What will you pay out-of-pocket, including premiums? Benefits—Are extra benefits and services, like eye exams or hearing aids covered? (These may be covered by some plans.) Doctor and hospital choice—Can you see the doctor(s) you want? Are they accepting new patients? Do you need a referral to see a specialist? Can you go to the hospital you want? Do you pay less to go to certain doctors or hospitals? Convenience—Where are the doctors’ offices? What are their hours? Is there paperwork? Travel—Do you spend part of each year in another state? Will the plan cover you there? Prescription drugs— What will your prescription drugs cost under the plan’s formulary (list of covered drugs)? What are your drug needs? Pharmacy choice—What pharmacies can you use? Quality of care—Quality of care varies among plans, doctors, hospitals, and other health care providers. Giving good quality health care means doing the right thing, at the right time, in the right way, for the right person—and getting the best possible results. Quality information to help you make the best choices for your well-being is available at www.medicare.gov on the web, or by calling 1-800-MEDICARE (1-800-633-4227).

Blue words in the text are defined on pages 97–100.

For more information about the Original Medicare Plan, see pages 25–32. Medicare Advantage Plans, see pages 33–42. ■ Medicare prescription drug coverage, see pages 43–56. ■ other Medicare plans, Government, and private insurance, see pages 57–62. joining and switching plans, see pages 71–78.

Do you have other health or prescription drug coverage? If you have or are eligible for other types of health or prescription coverage, read all the materials you get from your insurer or plan provider. Talk to your benefits administrator, insurer, or plan provider before you make any changes to your current coverage or you might lose your current coverage. Other types of coverage include employer or union coverage, TRICARE, the Department of Veterans Affairs (VA) benefits, coverage from a special program, or from a Medigap (Medicare Supplement Insurance) policy. Choosing among the Medicare options to get coverage that works for you is an important decision. You can get personalized help. 1 Visit www.medicare.gov on the web, and select “Search Tools” at the top of the page. 2 Call 1-800-MEDICARE (1-800-633-4227). Say “Agent” to speak to a customer service representative. TTY users should call 1-877-486-2048. 3 Call your State Health Insurance Assistance Program to get free counseling for your questions about appeals, buying other insurance, choosing a plan, buying a Medigap policy or other insurance, or Medicare rights and protections (see pages 92–95 for their telephone number). 4 Medicare works with many partners in your local community that can help you with these decisions.

Original Medicare Plan

What Is the Original Medicare Plan? The Original Medicare Plan is one of your health coverage choices as part of the Medicare Program. You will be in the Original Medicare Plan unless you choose to join a Medicare Advantage Plan (like an HMO or PPO). Most people get their coverage through the Original Medicare Plan.

How does the Original Medicare Plan work? The Original Medicare Plan is a fee-for-service plan that is managed by the Federal Government. The general rules for how the Original Medicare Plan works are below:

You use your red, white, and blue Medicare card when you get If you have Medicare Part A, you get all the medically-necessary Part A-covered services listed on page 9. If you have Medicare Part B, you get all the medically-necessary and preventive Part B-covered services listed on pages 13–19. You usually pay a monthly premium for Part B (see page 101 for the 2007 amount). You can go to any doctor, supplier, hospital, or other facility that is enrolled and accepts Medicare and is accepting new Medicare patients.

You pay a set amount for your health care (deductible)

before You may have a Medigap policy or other supplemental coverage that may pay deductibles, coinsurance, or other costs that aren’t covered by the Original Medicare Plan.

Blue words in the text are defined on pages 97–100.

Section 4: Original Medicare Plan ■ Every three months, you get a Medicare Summary Notice (MSN) in the mail if you got a Medicare-covered health care service during that period. The notice lists the details of the services you received and the amount you may be billed. These notices are sent by companies that handle bills for Medicare. If you disagree with the information on the MSN, you can file an appeal. Information on how to appeal is included on the notice. For more information about the MSN, visit www.medicare.gov on the web and select “Medicare Billing.” Or, call 1-800-MEDICARE (1-800-633-4227) and say “Billing.” Your costs in the Original Medicare Plan What you pay out-of-pocket depends on whether you have Part A and/or Part B (most people have both). whether your doctor or supplier accepts “assignment” (see page 27). how often you need health care. what type of health care you need. whether you choose to get services or supplies not covered by Medicare. In this case, you would pay all the costs for these services yourself. whether you have other health insurance that works with Medicare. whether you have Medicaid or get help paying your Medicare costs (see pages 66–67).

The lists on pages 101–104 shows what you pay in the Original Medicare Plan for common services in 2007. For details about these covered services, see page 9 for Part A and pages 13–19 for Part B. You can also visit www.medicare.gov on the web, or call 1-800-MEDICARE (1-800-633-4227). See Sections 7 and 8 for information about help to cover the costs that the Original Medicare Plan doesn’t cover. Section 4: Original Medicare Plan

What Is “Assignment” and Why Is it Important? Assignment is an agreement between you (the person with Medicare), doctors, other health care suppliers or providers, and Medicare. You “assign” Medicare to pay your doctor, supplier, or provider directly for care. Most doctors, suppliers, and providers accept assignment. If a doctor, other health care supplier, or provider accepts assignment, it means they agree to be paid by Medicare. agree to receive only the amount Medicare approves for their services. can only charge you, or other insurance you have, the Medicare deductible or coinsurance amount.

In some cases, doctors, other health care suppliers, and providers must accept assignment. For example, assignment must be accepted if you receive Medicare-covered physician assistant’s services. Doctors, other health care suppliers, and providers have to submit your claim to Medicare directly and can’t charge you for submitting the claim (this includes claims for glucose test strips). If the doctor, other health care supplier, or provider, doesn’t agree to accept assignment, they may charge you more than the Medicare-approved amount; however, for most services, there is a limit to what they can charge you. The highest amount you can be charged is called the “limiting charge.” The limiting charge is 15% over the Medicare-approved amount (but may be lower in your state). The limiting charge applies only to certain services and doesn’t apply to supplies and other durable medical equipment. In addition, you might have to pay the entire charge at the time of service. Medicare will send you payment for its share of the charge when the claim is processed. To get more information about assignment, visit www.medicare.gov on the web and select “Search Tools” at the top of the page. Then select “Find a Doctor.” You can also call 1-800-MEDICARE (1-800-633-4227).

Section 4: Original Medicare Plan Adding Prescription Drug Coverage to the Original Medicare Plan Medicare Prescription Drug Plans (Part D) People in the Original Medicare Plan can add drug coverage if they join a Medicare Prescription Drug Plan. They are available through private companies that work with Medicare to provide prescription coverage. See pages 43–56 for more details about Medicare prescription drug coverage. How does the Original Medicare Plan work with a Medicare Prescription Drug Plan? In most cases, you pay a separate monthly premium for your prescription drug plan. Premiums vary by plan. You pay a copayment or coinsurance and, in some cases, a yearly deductible for your prescription drugs. These charges vary by plan. You show a prescription card from your Medicare Prescription Drug Plan when you get your prescriptions filled. Medicare Prescription Drug Plans have contracts with pharmacies in your area. Check with the plan to make sure plan pharmacies are convenient to you. Some plans may offer a mail-order program that will allow you to have drugs sent directly to your home. Each Medicare drug plan has a list of covered drugs (formulary). The list must include at least two drugs (and in some cases all drugs) in all classes of drugs most commonly prescribed to people with Medicare. This makes sure that people with different medical conditions can get the treatment they need.

What if I can’t afford a Medicare Prescription Drug Plan? People with limited income and resources can qualify for extra help paying their Medicare Prescription Drug Plan costs. See pages 64–65 to find out if you may qualify for extra help.

If you have drug coverage through a previous or current employer or union, contact your benefits administrator before you make any changes to your prescription drug coverage. Joining a Part D plan could cause you to lose your, your spouse’s, and your dependent’s employer or union health and/or prescription coverage. Section 4: Original Medicare Plan

Buying a Medigap (Medicare Supplement Insurance) Policy The Original Medicare Plan pays for many health care services and supplies, but there are many costs it doesn’t cover. To help cover extra health care costs, you might want to buy a Medigap policy. Medicare doesn’t pay any of the costs for a Medigap policy. What is a Medigap policy? A Medigap policy is health insurance sold by private insurance companies to fill “gaps” in Original Medicare Plan coverage. Medigap policies help pay your share (coinsurance, copayments, or deductibles) of the costs of Medicare-covered services, and some policies cover certain costs not covered by the Original Medicare Plan. If you are in the Original Medicare Plan and have a Medigap policy, then Medicare and your Medigap policy will both pay their shares of covered health care costs. Insurance companies can only sell you a “standardized” Medigap policy. These Medigap policies must all have specific benefits. Generally, when you buy a Medigap policy you must have Medicare Part A and Part B. You or someone on your behalf (like a former employer or union) will have to pay the monthly Medicare Part B premium (see page 101 for the 2007 amount). You will also have to pay a premium to the Medigap insurance company. In most states, you may be able to choose from up to 12 different standardized Medigap policies (Medigap Plans A through L). Medigap policies must follow Federal and state laws. These laws protect you. A Medigap policy must be clearly identified as “Medicare Supplement Insurance.” Each Medigap Plan A through L has a different set of basic and extra benefits. In Massachusetts, Minnesota, and Wisconsin, plans are standardized in a different way. It’s important to compare Medigap policies because the benefits in any Medigap Plan A through L are the same for any insurance company, but the costs can vary a lot, and may go up as you get older. Each insurance company decides which Medigap policies it wants to sell and the price for each plan (with state review and approval).

Section 4: Original Medicare Plan What is a Medigap policy? (continued) Although some Medigap policies sold in the past covered prescription drugs, no new Medigap policies covering prescription drugs are being sold. To cover prescription drug costs, you may want to buy Medicare prescription drug coverage (Part D) offered by private companies approved by Medicare. If you join a Medicare Prescription Drug Plan, and your Medigap policy covers drugs, you must tell your Medigap insurer to remove the prescription drug coverage from your Medigap policy. If you and your spouse both want Medigap coverage, you each must buy separate Medigap policies. Your Medigap policy won’t cover any health care costs for your spouse. A Medigap policy only works with the Original Medicare Plan. Medigap policies generally provide some of the same kinds of supplemental coverage as Medicare Advantage Plans. If you join a Medicare Advantage Plan (like an HMO or PPO), your Medigap policy won’t work. This means it won’t pay any deductibles, copayments, or other cost-sharing under your Medicare Advantage Plan. Therefore, you may want to drop your Medigap policy if you join a Medicare Advantage Plan. However, you might not be able to get the same policy back, or in some cases, any policy if you leave the Medicare Advantage Plan. You have a legal right to keep the Medigap policy. Your rights to buy a Medigap policy may vary by state. If you already have a Medigap policy with prescription drug coverage, you can keep that policy with prescription drug coverage OR join a Medicare Prescription Drug Plan. Keep in mind that Medigap drug coverage is generally not as good as coverage under a Medicare drug plan. You pay all the costs for your Medigap drug coverage, but, if you join a Medicare Prescription Drug Plan, Medicare pays most of the cost for standard coverage. You may have to pay a premium. Medicare prescription drug coverage may cover more than the drug coverage in most Medigap policies. If you kept Medigap prescription drug coverage and didn’t join a Medicare drug plan when you were first eligible, you may have to pay a penalty if you choose to join later. You can’t have Medigap prescription drug coverage and Medicare prescription drug coverage at the same time. See page 43 for more information about your drug coverage choices. Section 4: Original Medicare Plan

What is a Medigap policy? (continued) For more information about Medigap policies, visit www.medicare.gov and view the booklet “Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare,” or call 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048.

If you have a limited income, there are programs that might help you pay costs Medicare doesn’t cover (see pages 63–70). How Your Bills Get Paid if You Have Other Health Insurance Sometimes your other insurance pays your health care bills first and the Original Medicare Plan pays second. Other insurance that must pay first includes employer or union group health plan coverage when coverage is based on your or a family member’s current employment, no-fault insurance (including automobile insurance), liability insurance (including automobile insurance), black lung benefits, and workers’ compensation.

It’s important that you tell your doctor, hospital, and pharmacy that you have other insurance so they know how to handle your bills. In some cases, if the insurance that is supposed to pay first doesn’t pay promptly, the Original Medicare Plan may make a “conditional” payment. This means it must be repaid to Medicare when a payment is made by the insurance that is supposed to pay first.

Section 4: Original Medicare Plan How Your Bills Get Paid if You Have Other Health Insurance (continued) If you are in the Original Medicare Plan and you have questions about who pays first, or you need to update your other health insurance information, call the Coordination of Benefits Contractor at 1-800-999-1118. TTY users should call 1-800-318-8782. For more information, visit www.medicare.gov on the web and view the booklet “Medicare and Other Health Benefits: Your Guide to Who Pays First” or call 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048.

If you join a Medicare Prescription Drug Plan, you must let your plan know if you have other prescription coverage. Other Options to Consider As you’ve read in this section, the Original Medicare Plan is a fee-forservice plan that covers many health care services. You can go to any doctor or hospital that accepts Medicare. Your Medicare decisions are important because they affect things like how much you pay and what is covered. Before making any decisions, learn as much as you can about the types of plans and coverage available to you. Here are other options you may want to consider: Medicare Advantage Plans (like an HMO or PPO) may offer a lower-cost alternative to the Original Medicare Plan, see pages 33–42. Medicare prescription drug coverage can be added to the Original Medicare Plan, see pages 43–56.

■ other types of Medicare plans, Government, and private insurance may be available to you, see pages 57–62.

Medicare Advantage Plans

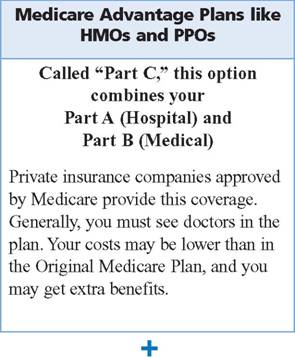

Blue words in the text are defined on pages 97–100. What Are Medicare Advantage Plans (like HMOs and PPOs)? Medicare Advantage Plans are health plan options that are approved by Medicare and run by private companies. They are part of the Medicare Program, and sometimes called “Part C.” When you join a Medicare Advantage Plan, you are still in Medicare. Some of these plans require referrals to see specialists. In many cases, the premiums or the costs of services (co-pays) can be lower in a Medicare Advantage Plan than they are in the Original Medicare Plan or the Original Medicare Plan with a Medigap policy. Medicare Advantage Plans provide all of your Part A (hospital) and Part B (medical) coverage and must cover medically-necessary services. They generally offer extra benefits, and many include Part D drug coverage. These plans often have networks, which means you may have to see doctors who belong to the plan or go to certain hospitals to get covered services. In many cases, your costs for services can be lower than in the Original Medicare Plan. Some of these plans coordinate your care, using networks and referrals, more than others. This can help manage your overall care and can also result in savings to you. Medicare pays an amount of money for your care every month to these private health plans, whether or not you use services. Medicare Advantage Plans also include options that provide specialized care for people who need a lot of health care services. Even if you are out of the service area of the plan, you are still covered for emergency (see page 15) or urgently needed care (see page 19). Medicare Advantage Plans include Medicare Preferred Provider Organization (PPO) Plans, see page 36, Medicare Health Maintenance Organization (HMO) Plans, see page 37, Medicare Private Fee-for-Service (PFFS) Plans, see page 37, Medicare Special Needs Plans, see page 38, and Medicare Medical Savings Account (MSA) Plans, see page 39.

Section 5: Medicare Advantage Plans Who Can Join? You can generally join if you live in the service area of the plan you want to join. In Medicare Health Maintenance Organization (HMO) Plans, the service area is also usually where you get services from the plan. Contact the plan to get more information about its service area. you have Medicare Part A and Part B. However, if you are already in a Medicare Advantage Plan and have only Part B, you may stay in your plan. you don’t have End-Stage Renal Disease (permanent kidney failure requiring dialysis or a kidney transplant), except as explained on page 74.

You have a chance to switch plans each year between November 15 and December 31. In certain situations, you may be able to switch plans at other times (see page 72). For more information about joining and switching plans, see pages 71–78. Visit www.medicare.gov on the web or call 1-800-MEDICARE (1-800-633-4227) to get help learning about and comparing plans in your area. TTY users should call 1-877-486-2048. Section 5: Medicare Advantage Plans If You Join...

you are still in the Medicare Program. you still have Medicare rights and protections (see pages 79–88). you still get complete Medicare Part A and Part B coverage (see pages 9 and 13–19). ■ you usually get prescription drug coverage (Part D) through the plan. In most Medicare Advantage Plans, if your plan offers Medicare prescription drug coverage and you want drug coverage, you must get it from your plan. In these cases, if you join a stand-alone Medicare Prescription Drug Plan, you will be disenrolled from your Medicare Advantage Plan. If you have a Medicare Private Fee-for-Service Plan that doesn’t offer Medicare prescription drug coverage, or if you have a Medicare Medical Savings Account Plan, you can also join a stand-alone Medicare Prescription Drug Plan (see page 43). you may be able to get extra benefits offered by the plan, such as coverage for vision, hearing, dental, and/or health and wellness programs. you still pay the Part B premium. You also pay the Medicare Advantage Plan’s premium that includes coverage for Part A and Part B benefits, prescription drug coverage (Part D if offered), and any other extra benefits (if offered). you usually will have to pay some other costs (such as copayments or coinsurance) for the services you get. Out-of-pocket costs in these plans are generally lower than in the Original Medicare Plan, but vary by the services you use. you don’t need to buy a Medigap (Medicare Supplement Insurance) policy. in some cases, your costs could be higher than the Original Medicare Plan, like if you see a doctor that doesn’t belong to the plan. every year in the fall, the plan will send you information about any changes in benefits, costs, or service areas.

Compare How Three Types of Medicare Advantage Plans Work Since each plan can vary, it’s important for you to read the plan materials carefully.

Note: If you have limited income and resources, you may qualify for help paying your health care costs (see pages 63–70).

Section 5: Medicare Advantage Plans

In most cases. If you want prescription drug Sometimes. If your plan doesn’t offer drug coverage, you must get it from the plan. The cost coverage, you can join a Medicare for coverage will be included in the premium. Prescription Drug Plan in your area. No. doctor to get a referral before you see any other health care provider. Yes. In most cases you must see a primary care No. You generally must get your care and In most cases. You can go to any Medicare-services from doctors or hospitals in the plan’s approved doctor or hospital that accepts the network (except emergency or urgent care). If the plan’s payment terms for covered services. plan has a Point-of-Service (POS) option, you can go out-of-network, but you will pay more than for services in-network. In most cases. Women don’t need a referral for a No. yearly screening mammogram or an in-network pap test and pelvic exam (at least every other year). • If your doctor leaves, your plan will notify PFFS plans are different from the Original you. You can choose another plan doctor. Medicare Plan. PFFS plans are offered by private companies. The private company, rather network, you may have to pay the full cost of • If you get health care outside the plan’s than Medicare, decides how much it will pay the services yourself. and what you pay for the services you get. Extra benefits are often offered for an extra • Follow the plan’s rules, like getting prior premium. authorization when needed. • Extra benefits are often offered for an extra premium.

Section 5: Medicare Advantage Plans How Medicare Advantage Plans Work (continued) The following types of health plans are also Medicare Advantage Plans. They are available in some areas to people who meet certain conditions. Medicare Special Needs Plans Medicare Special Needs Plans are specially designed for people with certain chronic diseases and other specialized health needs. These plans must provide all Medicare Part A and Part B health care and services. They also must provide Medicare prescription drug coverage (Part D). Generally, they offer extra benefits and may have lower copayments than the Original Medicare Plan. Medicare Special Needs Plans are designed to meet the needs of people who live in certain institutions (like a nursing home) or who continue to live at home, but require the same care as someone living in a nursing home, are eligible for both Medicare and Medicaid, or have one or more specific chronic or disabling conditions.

The plan may limit membership to people in one of these groups, but may enroll other people as well. A Medicare Special Needs Plan may help manage and coordinate the many services and providers their members use to help them stay healthy, follow their doctor’s orders related to diet and prescription drugs, and help coordinate coverage between Medicare and Medicaid. They may also identify a care coordinator to develop personal care plans to coordinate all health care provider efforts to meet the patient’s needs. For example, a Medicare Special Needs Plan for people with diabetes might use a care coordinator to help members monitor blood sugar, follow their diet, get proper exercise, get needed preventive services such as eye and foot exams, and get the right medicines to prevent complications. A Medicare Special Needs Plan for people with both Medicare and Medicaid might help members access community resources and coordinate many of their Medicare and Medicaid services. Visit www.medicare.gov on the web to get help learning about and comparing Medicare Special Needs Plans in your area. Select “Compare Health Plans and Medigap Policies in Your Area.” Or, call 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048.

Section 5: Medicare Advantage Plans

How Medicare Advantage Plans Work (continued) NEW Medicare Medical Savings Account Plans (MSAs) Medicare Medical Savings Account Plans (MSAs) are similar to Health Savings Account plans available outside of Medicare, and they have two parts. The first part is a Medicare Advantage Plan with a high deductible. This health plan won’t begin to pay covered costs until you have met the yearly deductible, which varies by plan. The second part is a Medical Savings Account into which Medicare deposits money that you may use to pay health care costs. For more information about Medicare MSA plans, visit www.medicare.gov on the web and view the booklet “Your Guide to Medicare Medical Savings Account Plans.” Or, call 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048.

Section 5: Medicare Advantage Plans Medicare Advantage Plans with Prescription Drug Coverage Most people with a Medicare Advantage Plan get prescription drug coverage through their plans. If you join a Medicare Advantage Plan and it offers this coverage, you must take the drug coverage your plan offers. Some Medicare Advantage Plans don’t include prescription drug coverage. Other options for getting drug coverage include joining another Medicare Advantage Plan that offers prescription drug coverage, or returning to the Original Medicare Plan and joining a stand-alone Medicare Prescription Drug Plan.

If you belong to a Medicare Advantage HMO or PPO, you can only get Medicare prescription drug coverage from your plan (if offered). If you join a stand-alone Medicare Prescription Drug Plan, you will be automatically disenrolled from your Medicare HMO or PPO and returned to the Original Medicare Plan. Your out-of-pocket costs depend on whether the plan charges a monthly premium in addition to your Part B premium (see page 101 for the 2007 amount). These plans charge one premium for Part A and Part B benefits, Part D prescription drug coverage (if offered), and extra benefits (if offered). whether the plan pays all or part of the monthly Part B premium (see page 41). whether the plan has a yearly deductible. how much you pay for each visit or service. the type of health care services you need and how often you get them. whether you follow the plan’s rules. the types of extra benefits you need, whether the plan covers extra benefits, and what it charges for them.

Extra benefits offered may help lower your overall out-of-pocket costs. To learn more about your costs in specific Medicare Advantage Plans, visit www.medicare.gov on the web, or call 1-800-MEDICARE (1-800-633-4227).

Section 5: Medicare Advantage Plans Saving on Your Medicare Part B Premium A few Medicare Advantage Plans may pay all or part of your Part B premium for you. You would still get all Part A and Part B-covered services. You can also call your State Medical Assistance (Medicaid) office to see if you can get help paying your Part B premium costs (see page 67). Saving on Your Prescription Drug Coverage Premium Your Medicare Advantage Plan’s premium may include the premium for Part B and for Part D (Medicare prescription drug coverage). Some Medicare Advantage Plans may pay all or part of the premium that pays for your prescription drug coverage. Read the plan materials carefully to see if the plan does this. Plans decide each year if they will reduce part or all of your prescription drug coverage premium. If you have limited income and resources, you may also be able to get extra help paying for your prescription drug costs (see pages 64–65).

How Your Bills Get Paid If You Have Other Sometimes your other insurance pays your health care bills first, and your Medicare Advantage Plan pays second. Other insurance that may pay first includes employer or union group health plan coverage (when coverage is based on your or a family member’s current employment), no-fault insurance (including automobile insurance), liability insurance (including automobile insurance), black lung benefits, and workers’ compensation.

Section 5: Medicare Advantage Plans How Your Bills Get Paid If You Have Other Health Insurance (continued) If you have other insurance, tell your doctor, hospital, and pharmacy so your bills get paid correctly. If you have questions about who pays first, or you need to update your other health insurance information, call the Coordination of Benefits Contractor at 1-800-999-1118. TTY users should call 1-800-318-8782. For more information about who pays first, visit www.medicare.gov on the web and view the booklet “Medicare and Other Health Benefits: Your Guide to Who Pays First,” or call 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048.

Other Options to Consider As you’ve read in this section, Medicare Advantage Plans are a way to get combined Medicare Part A and Part B benefits, and in most cases, prescription drug coverage (Part D). They may also provide more coordinated health care to help keep you healthy and lower your costs. Some plans (like HMOs) might use networks, where you may only be able to see certain doctors or go to certain hospitals. Your Medicare decisions are important because they affect things like how much you pay and what is covered. Before making any decisions, learn as much as you can about the types of plans and coverage available to you. Here are other options you may want to consider: Original Medicare Plan allows you to use any doctor or hospital that accepts Medicare, see pages 25–32. Medicare prescription drug coverage can be added to some Medicare Advantage Plans, see pages 43–56.

■ other Medicare plans, Government, and private insurance may be available to you, see pages 57–62. Medicare Prescription Drug Coverage

What is Medicare Prescription Drug Medicare offers prescription drug coverage for everyone with Medicare. This is called “Part D.” This coverage may help lower prescription drug costs and help protect against higher costs in the future. It can give you greater access to drugs that you can use to prevent complications of diseases and stay well.

If you join a Medicare drug plan, you usually pay a monthly premium. Part D is optional. If you decide not to enroll in a Medicare drug plan when you are first eligible, you may pay a penalty (see pages 47–48) if you choose to join later. These plans are run by insurance companies and other private companies approved by Medicare.

There are two ways to get Medicare prescription drug 1) Join a Medicare Prescription Drug Plan that adds drug coverage to the Original Medicare Plan, some Medicare Cost Plans, some Medicare Private Fee-for-Service Plans, and Medicare Medical Savings Account Plans. 2) Join a Medicare plan (like an HMO or PPO) that includes prescription drug coverage as part of the plan. You get all of your Medicare coverage through these plans, including prescription drugs.

Both types of plans are called Medicare drug plans in this Medicare offers help to employers and unions to help pay for prescription drug coverage. If you have employer or union drug coverage, see page 61. Joining a Part D plan could end the retiree health benefits you and your family get. Talk to your benefits administrator. Blue words in the text are defined on pages 97–100.

How does it work? After you have joined the Medicare drug plan you want, the plan will mail you membership materials including a plan member card you use when you get your prescriptions filled. When you use the card, you will pay the copayment, coinsurance, and/or deductible, if any. In Medicare Advantage Plans that include Medicare prescription drug coverage (Part D), your health care and drug usage is coordinated, with an emphasis on preventive care to keep you healthy. How much does it cost? Most drug plans charge a monthly premium that varies by plan. You pay this in addition to the Part B premium. Some drug plans charge no premium. If you have limited income and resources, you may get extra help to cover prescription drugs for little or no cost (see pages 64–65). Your costs will vary depending on which drugs you use, which Medicare drug plan you choose, and whether you get extra help paying your Part D costs. Having a variety of plans to choose from gives you the chance to pick a plan that meets your unique needs. Choosing a plan that fits your situation allows you to get the coverage you want at the best price possible. If you belong to a Medicare Advantage Plan (like an HMO or PPO) or a Medicare Cost Plan that offers Medicare prescription drug coverage, the monthly premium you pay to the plan includes an amount for prescription drug coverage. Some plans charge no premium. You may be able to pick a plan with or without a monthly premium, deductible or coverage gap. To find the actual costs of the Medicare drug and health plans in your area, visit www.medicare.gov on the web. Select “Compare Medicare Prescription Drug Plans.” Or, call 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048. Section 6: Medicare Prescription Drug Coverage

What is a coverage gap? Medicare drug plans may have a “coverage gap,” which is sometimes called the “donut hole.” A coverage gap means that after you and your plan have spent a certain amount of money for covered drugs (no more than $2,400), you have to pay out-of-pocket all costs for your drugs while you are in the “gap.” The most you have to pay out-of-pocket in the coverage gap is $3,051.25. This amount doesn’t include your plan’s monthly premium that you must continue to pay even while you are in the coverage gap. Once you’ve reached your plan’s out-of-pocket limit, you will have “catastrophic coverage.” This means that you only pay a coinsurance amount (like 5% of the drug cost) or a copayment (like $2.15 or $5.35 for each prescription) for the rest of the calendar year. Note: If you get extra help paying your drug costs, you won’t have a coverage gap. However, you will probably have to pay a small copayment or coinsurance amount.

How to Compare Medicare Drug Plans Each Medicare drug plan is different. When you choose a Medicare drug plan for the first time, or switch to a different Medicare drug plan, you should compare the plans in your area and choose one that meets your cost and coverage needs. Get personalized help comparing Medicare prescription drug coverage: Visit www.medicare.gov on the web. Select “Compare Medicare Prescription Drug Plans.” Call 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048. Call your State Health Insurance Assistance Program (see pages 92–95 for their telephone number).

Have your Medicare card, a list of your drugs and their dosage, and the name of the pharmacy you use available. Look at the following to compare plans in your area. Drug Coverage. Plans may have rules about what drugs are covered in different categories. Check to see if the plan covers your prescription drugs. Medicare drug plans will have a list of drugs covered by the plan (formulary) that must always meet Medicare’s requirements. Even if a drug is on the plan’s list, there may be special rules for filling the prescription. But, the list can change during the year because drug therapies change, and new drugs and medical knowledge become available. If you are affected by the change, your plan will notify you at least 60 days before the formulary changes. If there is a formulary change that affects a drug you take, in most cases, it will still be covered for you until the end of the year. Cost. Check to see how much your prescription drugs would cost in each plan. If you currently have prescription drug coverage, compare your current costs to those of the Medicare drug plans you are considering. Monthly premiums, deductibles, and your share of the cost of your prescriptions (copayments and/or coinsurance) will vary with each plan and by each drug. If you have limited income or resources, you may qualify for “extra help” paying your drug plan costs (see pages 64–65). Convenience. Medicare drug plans must contract with pharmacies in your area. Check with the plan to make sure the pharmacies in the plan are the ones you want to use. Some plans also allow you to get your prescriptions through the mail. If you spend part of the year in another state, see if the plan will cover you there.

Section 6: Medicare Prescription Drug Coverage

Choosing Medicare Prescription Drug Coverage for the First Time Like other insurance, Medicare prescription drug coverage will be there when you need it to help you with drug costs. Even if you don’t take a lot of prescription drugs now, you still should consider joining a Medicare drug plan. As we age, most people need prescription drugs to stay healthy. Are you new to Medicare, or have you lost creditable prescription drug coverage (coverage expected to pay at least as much as standard Medicare prescription drug coverage, like that provided by some employer or union plans) within the last 63 days?

If so, joining now means you will pay your lowest possible monthly premium. Every year (from November 15—December 31), you can switch to a different Medicare drug plan if your needs change. You can join a Medicare drug plan from three months before you turn 65 to three months after you turn 65 (called your Initial Enrollment Period). Generally, if you are disabled, you can join three months before and three months after your 25th month of disability. The plan will notify you when your coverage begins.

If you don’t join a Medicare drug plan when you are first eligible to join (during your Initial Enrollment Period), and there is a period of 63 continuous days or more during which you don’t have creditable prescription drug coverage, you may have to pay a late enrollment penalty when you do join. This amount changes every year. You will have to pay a penalty as long as you have Medicare prescription drug coverage.

How much will my penalty be? Your penalty is calculated when you first join a Medicare drug plan. To estimate your penalty, take 1% of the national average premium for the year you join (the 2007 amounts are on page 104). Multiply it by the number of full months you were eligible to join a Medicare drug plan but didn’t. This is your estimated penalty amount, which is added each month to your Medicare drug plan’s premium for as long as you have a plan. If you qualify for extra help, the penalty will be different. For help figuring your penalty amount, call 1-800-MEDICARE (1-800-633-4227) or your State Health Insurance Assistance Program (see pages 92–95 for their telephone number). Switching Medicare Prescription Drug Plans If you currently have Medicare prescription drug coverage, you should review your coverage each year in the fall. You might want to switch Medicare drug plans if another plan better meets your needs. Generally, you can only switch plans from November 15—December 31 of each year (see pages 71–78). Coverage under the new plan will begin January 1 of the following year. It’s best to join a plan early in the month once you’ve made your decision. In certain cases, you may be able to change plans at other times (see page 72). If you are happy with your coverage, and your Medicare drug plan is still offered in your area, you don’t have to do anything for your coverage to continue.

Only give personal information to doctors, other providers, and Medicare plans approved by Medicare, and to the people in your community who work with Medicare, like your State Health Insurance Assistance Program or Social Security (SSA). Call 1-800-MEDICARE (1-800-633-4227) if you have questions. TTY users should call 1-877-486-2048.

Section 6: Medicare Prescription Drug Coverage

What if I have full coverage from my state Medicaid program? If you have full coverage from your state Medicaid program and you are eligible for Medicare, Medicare will automatically enroll you in Medicare prescription drug coverage if you have not already chosen to do so. Medicare, not Medicaid, will provide your drug coverage and start paying for your prescription drugs. Medicaid will still cover other care that Medicare doesn’t cover. In some limited cases, Medicaid will add to Medicare drug coverage. You can switch to another Medicare drug plan each month. Medicare pays for almost all of the cost of your covered drugs if you join a Medicare Prescription Drug Plan or a Medicare Advantage Plan with Medicare prescription drug coverage. In most cases, you will pay only a small amount out-of-pocket for each covered prescription. Your costs and the drugs that are covered vary by plan. If you have Medicare and full coverage from Medicaid, and you live in certain institutions (like a nursing home), you will pay nothing for your covered prescription drugs. What if I get certain benefits or other help to pay Medicare costs? If you don’t join a Medicare drug plan, Medicare will enroll you in one to make sure you get help paying for your prescription drug costs. You will get extensive drug coverage with little or no monthly premium. Generally, you pay only a small amount out-of-pocket for each covered prescription. If you apply and qualify for extra help paying your Medicare costs or get Supplemental Security Income (SSI) benefits without Medicaid, you can switch plans once by the end of the calendar year, and once each year after between November 15 and December 31. If you belong to a Medicare Savings Program (your state Medicaid program pays your Medicare premiums), you can switch to another Medicare drug plan at any time.

If you have other prescription drug coverage that’s at least as good as Medicare’s drug coverage (creditable prescription drug coverage), you can decline to keep the drug plan Medicare enrolls you in. If you don’t want to join this plan or any Medicare drug plan, call 1-800-MEDICARE (1-800-633-4227), or call the plan Medicare enrolls you in.

What if I have prescription drug coverage from a former or current employer or union? Medicare offers employers and unions help paying for retiree drug coverage. Your (or your spouse’s) former or current employer or union must notify you about how your current coverage compares to Medicare’s (minimum) standard prescription drug coverage. Employers or unions may provide this information within a notice or in your benefits handbook. Keep this notice because it can help you decide whether to join a Medicare drug plan. It is your proof of creditable prescription drug coverage. You won’t have to pay a penalty if your employer or union stops offering prescription drug coverage that was creditable coverage if you join a Medicare drug plan before going 63 days without coverage. If your employer or union drug coverage isn’t as good as Medicare prescription drug coverage (isn’t creditable prescription drug coverage), find out about your options from your benefits administrator. You will have several choices. If you aren’t notified, contact your benefits administrator.

If you drop your employer or union coverage, you may not be able to get it back. You also may not be able to drop your employer or union drug coverage without also dropping your employer or union health (doctor and hospital) coverage. If you drop your employer or union coverage for yourself, you may also have to drop coverage for your spouse and dependents. Contact your benefits administrator before you make any change to your drug coverage. Section 6: Medicare Prescription Drug Coverage

What if I get prescription drug coverage from TRICARE, the Department of Veterans Affairs (VA), or the Federal Employee Health Benefits Program (FEHBP)? As long as they still qualify, most people keep their TRICARE, VA, or FEHBP prescription drug coverage. Contact your benefits administrator or your insurer for information about your TRICARE, VA, or FEHBP coverage before making any changes. It will almost always be to your advantage to keep your current coverage without any changes. However, in some cases, adding Medicare prescription drug coverage can provide you with extra coverage and, sometimes, lower copayments. If you lose your TRICARE, VA, or FEHBP coverage and your Medicare drug coverage begins within 63 days, in most cases, you won’t have to pay a penalty.